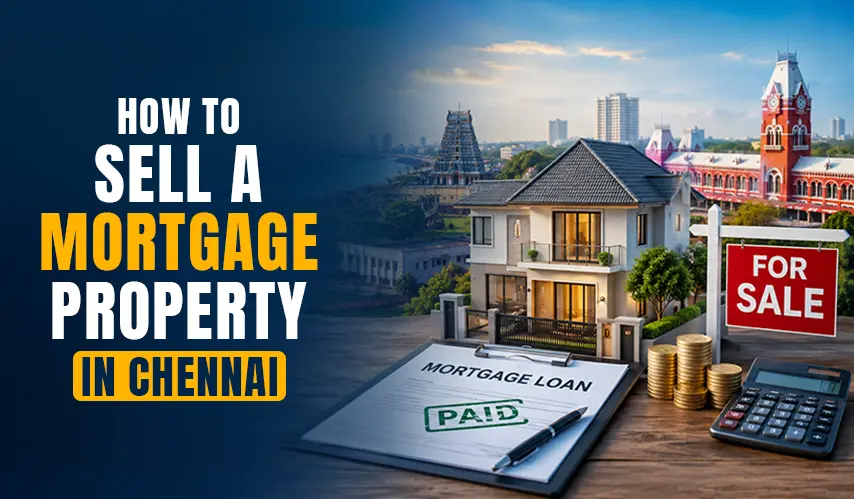

Selling a property can be a pretty straightforward thing, especially when all documents are clear and there are no financial ties attached. But a lot of homeowners in Chennai kind of ask the same question again and again: can they sell a property that is still under a home loan or a mortgage? The good news is that selling a mortgaged property in Chennai is completely legal, and it is also possible, but only if you stick to the correct procedures and make sure the pending loan amount gets settled.

Whether you have an apartment, a villa, an independent house, or even plots in ECR that you purchased using a home loan, getting the full picture on how it works can help you avoid last-minute delays and keep the whole deal moving smoothly.

Can You Sell a Mortgaged Property?

Yes, you can sell a mortgaged property, even if the home loan hasn’t been paid off, it’s just that usually the lender doesn’t let it happen in a simple way. Basically, the mortgage is still on the file. But property ownership can still be transferred; only, the outstanding mortgage has to be cleared first. Usually, the property papers and documents are kept by the bank or the financial institution, since they work as security for the loan, so the bank typically needs to release or remove the mortgage before the sale can go through.

In Chennai, many property dealings involve a mortgage property, so it’s more or less a common thing in the real estate market.

Understanding the Mortgage Status

Before you list your property for sale, the first step is, kind of, to get clear on what your current loan status actually is.

You should gather:

Go ahead and contact your bank, ask for an updated statement that shows the exact figure required to close the loan. Having that number upfront will help you manage the sale process more efficiently and with less guessing.

Let the Buyer Know About the Mortgage

Being straight up matters a lot when you’re selling a property that still has a mortgage on it. Honestly some sellers try to keep the home loan details a bit vague, and that can later spark trust problems.

It’s better to tell potential buyers clearly, like:

The property is currently under a home loan

The lender balance will be paid off as part of the sale process

The legal ownership papers will be handed over once the loan is officially cleared

Most buyers already know how these transactions work, and they usually don’t raise concerns, as long as everything is managed properly.

Methods to Sell a Mortgaged Property

Seller Pays off the Mortgage Before the Sale This approach is the most straightforward.

If you have enough savings or other alternative money, you can clear the balance of the loan first, before you list and sell the property.

After the loan is officially finished:

The bank releases the original documents.

The mortgage gets removed.

The house or apartments in Chennai become free of financial encumbrances.

Because of that the whole sale goes smoother, and buyers tend to feel more comfortable with it.

Buyer pays the remaining loan amount

In many situations, the buyer agrees to remit part of the transaction value straight to the bank, kind of yes, without too much back and forth.

The sequence usually looks like this:

Buyer pays the outstanding loan sum to the lender.

Bank closes the loan.

The original documents are handed over.

The rest of the money is then paid to the seller.

Property registration gets completed.

This approach is among the more normal methods you’ll see across the Chennai real estate market.

Loan transfer to the buyer’s bank

If the buyer is also arranging a home loan, the buyer’s bank and the seller’s bank will coordinate the deal, kind of back and forth, so it runs smoothly.

The buyer’s bank usually does the following things :

Pays off the seller’s loan that is still outstanding.

Collects the original papers or documents from the seller’s bank.

Handles the buyer’s home loan, then confirms it properly.

Finalizes the ownership transfer and completion steps.

This approach is pretty common for high-value residential homes, especially when the amount involved is large enough that both banks need to stay in sync.

Documents You’ll Need to Sell a Property That’s Still Under Mortgage

To make sure it goes smoothly, keep these papers with you, and try not to leave it till the end. You should have:

Once you keep everything handy, it helps the buyer feel more assured , and the entire process can move faster.

Get a No Objection Certificate (NOC)

Once the pending loan is settled, the bank will issue something like a

These papers serve as proof that the home loan is fully cleared and that the financial institution no longer has any sort of claim on the property, at all.

Often buyers ask for these certificates before they even move forward with registration, because they want to be sure everything is tied up properly.

Check the Encumbrance Certificate

After the loan closure, maybe obtain an updated Encumbrance Certificate (EC), so you can verify that the mortgage entry got removed.

An EC is one of the most important legal documents for property dealings; it basically assures buyers that the property is free from financial liabilities.

In Chennai, buyers usually insist on checking the most recent EC before finalizing the purchase, because it feels safer that way.

Get a sense of the Tax Implications first

When you sell a property in chennai, you might face capital gains tax; it really depends on a few things, like the original purchase cost, the eventual sale price , how long you kept the place, and which exemptions could apply.

If you have owned the property for more than two years, it may count as a longterm capital asset, so that could change the tax treatment.

It’s smart to talk with a Chartered Accountant or a tax advisor to sort out things such as your possible capital gains tax exposure, what exemptions you can actually use, and whether there are reinvestment advantages available.

With a bit of tax planning , you can often help stretch and maximize your returns once the sale is done. Pricing your property the right way

One of the most common mistakes sellers do is set too high the price on their mortgaged property, like really high.

If you want to attract actual buyers (not just curious visitors), then:

Look at current market trends

Compare similar properties nearby (same neighborhood, similar size)

Factor in the property's age, its condition, and the location.

When you go for a realistic number, the whole selling timeline can shrink a lot, and yes it can be noticeably faster than you expect.

Final Thoughts

Selling a mortgaged property in Chennai can feel a little tangled at first, but honestly, if you plan ahead in the right way, it usually goes through smoothly legally. The main part is simple, you need to know where your loan stands, stay open with the buyer, clear any pending dues, and have all papers on hand, right from the start.

Whether you decide to close the loan yourself or settle the balance using the sale proceeds, sticking to the proper workflow will reduce the chances of delays and those pesky legal issues that pop up.

Also, Chennai real estate keeps growing, the demand for solid homes is also rising, so a well-priced property that is properly documented tends to pull in real buyers. When you handle the steps correctly, you can sell your mortgaged property with more confidence and still aim for the best possible value on your investment.